Tailored To Your Needs

Manufactured Home insurance

Manufactured Home Insurance Own or rent, It doesn’t matter, We’ll have you covered in times of disaster. Protection You Trust.

Manufactured Home Insurance, if you own or are in the market for a manufactured home, you might wonder how your Manufactured home insurance compares to a traditional homeowners policy. We’ll shed some light on the key risks specific to such homes and how they might affect your mobile home insurance coverage.

What is a manufactured home, anyway?

If the term is unfamiliar, it’s essentially another way to describe a mobile home. According to the U.S. Department of Housing and Urban Development, the official definition of a manufactured home is a house that is built in an assembly plant — in compliance with strict design and safety codes — and transported on a portable chassis to its ultimate destination. And manufactured home insurance doesn’t just protect your home — it also covers detached structures like garages and sheds.

Insurance protection for manufactured homes.

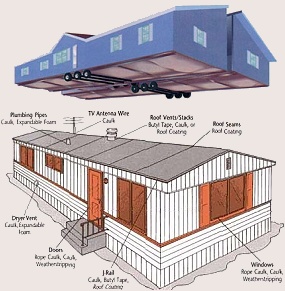

Arranging the smartest mobile home policy means knowing the areas in which your abode is most vulnerable.

Firehttp://www.safeconow.com

According to the National Fire Protection Association, the top cause of fires in manufactured homes is electrical distribution equipment. In the majority of other homes, though, cooking is the top threat.

Why is this noteworthy? Mostly because it means mobile-home fires can occur more easily when no one is home, allowing the damage to spread unimpeded. To make matters worse, smoke alarms are missing in half of all manufactured homes, according to the National Fire Protection Association.

Adding ample amounts of Manufactured home insurance, dwelling protection (which covers your home’s structure and personal property insurance which pays to replace your possessions lost in a blaze) is a great way to gain some extra peace of mind.

Insulation

While manufactured homes have come a long way over the years, the differences in construction between site-built homes and traditional homes can still bring about some insurance issues one of which is insulation. You could also explore winterizing or insulating your mobile home yourself to further decrease your risk.

Wind

One of the most common concerns your insurer may have regarding your manufactured home is damage from heavy windstorms. If your place is lighter than most site-built homes and is at risk of blowing over, you might feel more comfortable with increased limits on your Manufactured home insurance, dwelling protection, in case you need to repair your home in the specific instances it’s damaged by wind or hail.

Collision

While your manufactured home will be your residence for years, it’s still mobile for one day. Adding some form of trip collision coverage will help make sure you’re prepared if the unthinkable happens and your home is totaled while being transported from the assembly plant to its destination.

Manufactured home depreciation

Another key aspect to bear in mind with your manufactured home Insurance policy is the depreciation on mobile homes as they age. This could mean the value of your home might have gone down since you first started your insurance policy, and your limits on dwelling protection and liability coverage (not to mention your overall premium) are higher than they need to be.

It’s always wise to reevaluate your home and your assets every so often to make sure you’re getting the most from your manufactured home insurance.

Have more homeowners insurance questions?

Check out more details on coverage, limits, and responsibilities to help you get the best mobile home insurance quote.

Manufactured Home Insurance, Another term for mobile home insurance, Getting your mobile home insurance may seem confusing, but it doesn’t have to be. In order to make sense of it all you may want to review some of the more common questions other mobile home owners have asked about insurance coverage. This may be one of the best ways to get a better understanding as well as get the perfect policy for your individual needs.

Will my manufactured home insurance cover my belongings? Generally this depends on the type of manufactured home coverage you get. You can certainly get coverage for personal possessions included. If you currently have a mobile home policy for insurance you should make sure your belongings are actually covered instead of assuming they are.

Are decks, garages and storage sheds included in my policy? Again this depends on the type and amount of manufactured home insurance you get. Obviously, you can get basic coverage to take of nothing more than the manufactured home itself. In most cases, owners prefer to get coverage so they can have their belongings, attached structures and detached structures all covered.

If I am only renting a mobile home should I get insurance? By all means! Of course, if you are not the owner you will probably only need contents insurance. However, you may want to be sure your landlord has mobile home coverage on the home before renting from him or her. You can never have too much manufactured home insurance coverage.

What’s the difference between replacement cost and actual cash value? Often times, people sign up for mobile home insurance coverage without realizing what exactly they are getting. It is important to look at more than the bottom line when it comes to premium costs because you want to get all the coverage you need.

Replacement cost coverage means if you should lose your home or possessions you will get the cost or close to it to replace those items for a current market equivalent.

Actual Cash Value takes depreciation into account and offers you only what your home or items may be worth after depreciation. Though you will generally save on monthly premiums for choosing actual cash value, you will probably have to come up with a good deal of money out of your pocket to pay the difference if you want similar items or a mobile home up to the standards you are hoping for.https://www.easterninsuranceinc.com [contact-form-7 404 "Not Found"]

If you are financing your mobile home you may be required to meet certain guidelines set in place by the lender for your manufactured home insurance.

What type of insurance may be more difficult to get? Depending on the area you live in, it may be more differcult to get coverage for tornadoes, floods or even earthquakes. Find out what your policy currently covers to make sure you get what you need to protect yourself.

How can I lower my rates? When it comes to buying manufactured homes insurance there are numerous ways you can help save money. Some examples include improving the safety with reinforced roof beams and storm shutters.

MANUFACTURED HOME INSURANCE